Tax season is here, and we just received our annual mortgage interest statement from our bank. It is somewhat depressing to see how much money went to pay interest on our loan, but cool thing about it this year is that we paid about half as much in interest than we did last year.

As I wrote last year, one of our goals was to pay down our mortgage. We succeeded by paying 34% of it off. This not only reduced our balance, but also reduced the monthly interest, with a larger portion going towards the principal payment every month.

But, What About the Tax Deduction?

I have heard on several occasions the advice that I should keep my mortgage around so that I can get a tax deduction. I believed this for many years, but in 2009, I was shown some real math that put it into perspective. The math I was shown was very simplified compared to where we are going to go here, but since then I have paid a tiny bit more attention to how taxes work, so I want to walk through how the math works out at a slightly higher level.

There are two basic things that can reduce your tax bill - deductions and exemptions. Deductions are further broken down by "above the line" deductions, and "below the line" or itemized deductions. Above the line deductions will always lower your income (to produce the "line" - the Adjusted Gross Income, or AGI), whereas "below the line" deductions have to compete against the "standard deduction." This article goes in a bit more detail on these, which I will summarize here. The math looks like this:

- Take your total income

- Subtract your above the line deductions (IRA contributions, student loan interest, HSA contributions)

- You now have your AGI

- Total up all of your itemized deductions (mortgage interest, charitable contributions, business expenses, etc), and then subtract either that total, or the "standard deduction", whichever is higher.

- Subtract any exemptions (personal exemption is $3,950 per person)

- You now have your taxable income. Compute your tax bill based on the progressive brackets.

- Subtract any credits (child tax credit of up to $1,000 per child, varies with income)

- You have your final bill

Let's use some example numbers. Let's say a family of 4 earned $80,000 per year, and made no above the line deductions. At $80,000, this puts them in the 25% tax bracket. But that doesn't mean the government takes 25% of their $80k. The "progressive" tax system is such that the 25% is taken out of everything above $73,800. They take 10% of everything under 18,150, then 15% of everything up to 73,800, then 25% of everything over 73,800. For our example family, $80,000 starts the tax bill out at $11,712.50.

$11,712.50 is not what they will end up paying in taxes. They have no above the line deductions, so their AGI is $80,000. As a family, their standard deduction is $12,400, so that drops their taxable income to $67,600. They have 2 children, for a total of 4 personal exemptions, another $15,800, bringing their total of $51,800. This is in the 15% tax bracket, and with the progressive rate they end up with a tax bill of $6,866. After subtracting $2,000 for the child tax credit, their final bill is $4,866.

Wait, we were talking about mortgages

We now have a simple tax bill computed for our example family. Noticed I used the standard deduction of $12,400. Many families will use this, as it is likely higher than their itemized deductions. Itemized deductions usually consist mostly of charitable contributions and mortgage interest, and depending on the state, state and local taxes (income, real estate, property and sales) as well. If you bought a car and paid $2,000 in sales tax, that would qualify as an itemized deduction, as would every time you ate out or bought things (if you like to keep track of your receipts).

Back to the example family. If they only had their $2k mortgage interest and gave away 10% ($8k), their itemized deduction would be less than the standard deduction. In this case, it doesn't matter if they had their mortgage or not. If they paid their mortgage off early, or kept it, the result would be the same - they would still take the standard deduction.

What if instead of $2k in interest they had $8k. Instead of paying $4,866 in taxes with the standard deduction, they pay $4,326. Feel free to check the math using Tax Act's calculator.

By spending $8,000 in interest, they saved $540 on their taxes.

Let that math sink in - they gave a bank $8,000, to save from sending $540 to the government.

| Standard Deduction | Itemized | |

| Income | $80,000 | $80,000 |

| Above the Line Deductions | $0 | $0 |

| AGI | $80,000 | $80,000 |

| Deductions | $12,400 | $10,000 |

| Exemptions | $15,800 | $15,800 |

| Tax bill | $6,866 | $7,222.50 |

| After Credits | $4,866 | $5,222.50 |

A Lower Income Example

$80,000 is a bit high, so lets go a bit lower. In 2013, the median US income was about $50,000. They have a $130,000 mortgage at 4.25% for 30 years, and have a total house payment (including taxes) just shy of 1/4th of their take home pay. They pay over $5,000 in interest the first four years of the loan - 10% of their income. They also try to give away 10% every year, giving them $10,000 in deductions. This too is shy of the $12,400 standard deduction. In order for them to push past that, they would need over $7,400 in interest - which they could do with a $180,000 house with 0% down.

A Higher Income Example

Finally, there is another family with 2 children who earned $100,000 per year. They are a little more generous and give away, or otherwise have deductions that amount to, 12.4% of their income. This puts their deduction right at the same level as the standard deduction. They have a more reasonable mortgage and have paid it down some, and are spending about $2,000 in interest per year. With just the standard deduction, their tax bill would be $7,866. With the $2,000 in interest, their tax bill drops by $300 to $7,566. If they were to pay their mortgage off, they would pay the full $7,866 in taxes after the standard deduction. But, they would have saved themselves from sending $2,000 to a bank, netting them $1,700 in savings over that year.

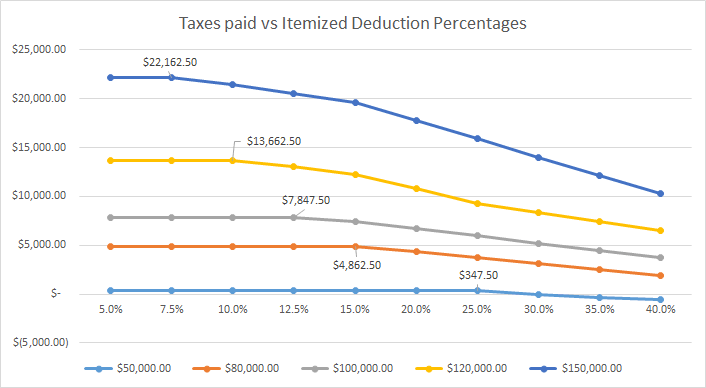

Look, a Chart

My Excel charting skills arent the greatest, but here is a chart depicting the points for various income levels where itemized deductions, as a percentage of income, start to outweigh the standard deduction. I included income levels from $50k to $150k, because that range is the least complicated for a married family with 2 children. Below that you run into additional child tax credits and EITC. Above that you really see the child tax credit really start to disappear (it starts to phase out at $110,000), and even higher you get into the Alternative Minimum Tax (AMT). Above the line deductions, and all credits were held constant. Only the amount of itemized deductions were changed.

For a family earning $120,000, they would need to have deductions of about 10% or more of their income to start reducing their tax bill. Up until that point, they owe $13,662.50 in federal taxes.

For a median-income family of $50k, to reduce their tax bill of $347.00, they would need to itemize away more than 25% of their income.

Do the Math

If you have been told to keep your mortgage for the sake of getting a tax deduction, I want you to look at your taxes this year and ask yourself - is that statement really true?

If you find yourself taking the standard deduction, then paying interest on your mortgage is not saving you anything on your taxes.

If your total deductions are more than standard deduction, find out how much you are truly saving on your taxes by having the mortgage interest. Ask yourself - am I saving more in taxes than I am sending to the bank? If the answer is no, then the mortgage is not doing you any favors.

If you want to run some numbers, there is a good calculator by Tax Act, and another one here.

And if you really don't want the government to take so much of your money in taxes, you have two good options for doing so - donate to reputable charities, or have more kids. The later is likely the bigger challenge, and as is the case for taking out a mortgage solely for having a tax deduction, I would advise against having multiple children solely for gaining tax credits and exemptions.